Personal Finance: A Beginner’s Roadmap

Personal Finance: A Beginner’s Roadmap

Money plays an important role in everyone’s life. Whether you’re a student, a working professional, or someone planning for retirement, understanding personal finance is one of the most valuable skills you can develop. Unfortunately, many people are never taught how to manage their money effectively. As a result, they struggle with debt, lack savings, and feel financially stressed.

The good news is that learning personal finance doesn’t require a finance degree. By understanding a few basic principles and following a clear roadmap, anyone can build a strong financial future.

In this beginner’s guide, you’ll learn the fundamentals of personal finance, why it matters, and the essential habits that can help you take control of your money.

What Is Personal Finance?

Personal finance refers to the process of managing your money to achieve your financial goals. It includes earning income, budgeting, saving, investing, managing debt, planning taxes, and preparing for retirement.

Simply put, personal finance is about making smart financial decisions every day.

For a detailed explanation of personal finance, you can visit:

https://www.investopedia.com/personal-finance-4427760

Managing your finances effectively allows you to:

- Pay bills on time

- Build savings

- Avoid unnecessary debt

- Invest wisely

- Prepare for emergencies

- Achieve long-term financial security

Personal finance is not about becoming rich overnight. Instead, it’s about developing healthy money habits that improve your financial well-being over time.

Why Personal Finance Matters

Many people earn a good salary but still struggle financially because they don’t know how to manage their money.

Learning personal finance helps you:

1. Reduce Financial Stress

Money problems are one of the leading causes of stress worldwide. Having a financial plan gives you confidence and peace of mind.

2. Prepare for Emergencies

Unexpected expenses like medical bills, car repairs, or job loss can happen at any time. A good financial plan ensures you’re prepared.

3. Achieve Financial Goals

Whether you want to buy a home, travel the world, or start a business, personal finance helps turn those dreams into achievable goals.

4. Avoid Debt

Good money management prevents overspending and reduces dependence on credit cards or loans.

5. Build Long-Term Wealth

Small financial decisions made consistently over many years can create significant wealth through saving and investing.

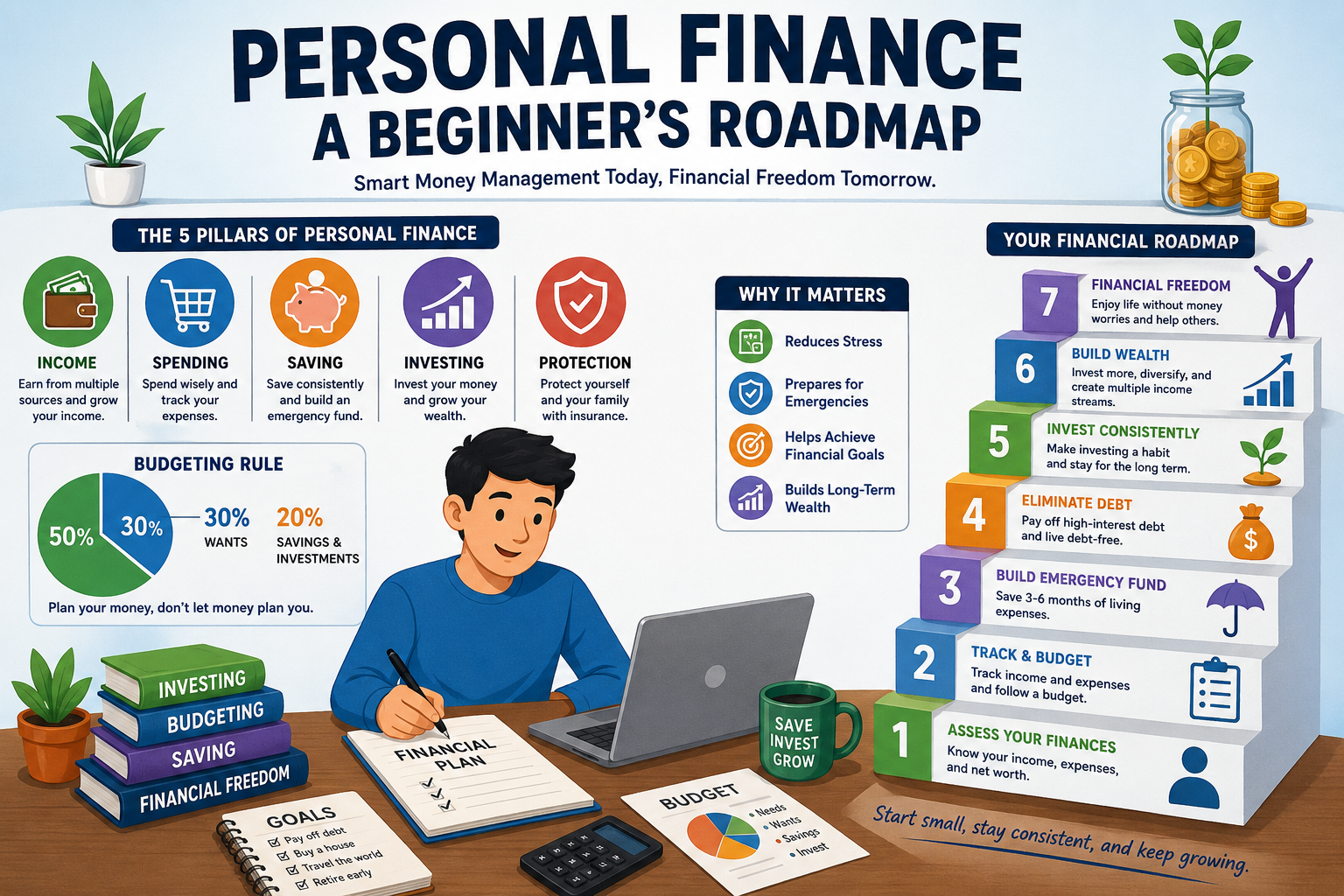

The Five Pillars of Personal Finance

Understanding the five core areas of personal finance makes managing money much easier.

1. Income

Income is the money you earn from different sources.

Examples include:

- Salary

- Freelancing

- Business profits

- Rental income

- Investment dividends

- Side hustles

The first step in personal finance is increasing and managing your income wisely.

2. Spending

Spending is where most financial mistakes happen.

Many people spend more than they earn because they don’t track their expenses.

Instead of asking:

“Can I afford this?”

Ask:

“Is this purchase helping me reach my financial goals?”

Tracking expenses helps identify unnecessary spending and improve financial habits.

3. Saving

Saving means setting aside money for future needs.

Savings can help you:

- Handle emergencies

- Make large purchases

- Reduce financial stress

- Achieve financial independence

Experts recommend saving at least 20% of your monthly income whenever possible.

4. Investing

Saving protects your money.

Investing helps your money grow.

Investments may include:

- Stocks

- Bonds

- Mutual Funds

- ETFs

- Real Estate

We’ll discuss beginner investing in Part 2.

To learn investment basics, visit:

https://www.investor.gov/introduction-investing

5. Protection

Financial protection includes:

- Health insurance

- Life insurance

- Disability insurance

- Emergency funds

Protection reduces financial risk when unexpected situations occur.

Budgeting: The Foundation of Personal Finance

A budget is simply a plan for your money.

It tells every dollar where it should go before you spend it.

Without a budget, it’s easy to lose track of spending.

Budgeting doesn’t mean limiting your life—it means spending intentionally.

How to Create a Budget

Step 1: Calculate Monthly Income

Include every reliable source of income.

Example:

Salary: $3,500

Freelancing: $500

Total Income = $4,000

Step 2: List Monthly Expenses

Separate expenses into two categories.

Fixed Expenses

- Rent

- Mortgage

- Insurance

- Internet

- Loan payments

Variable Expenses

- Food

- Entertainment

- Shopping

- Fuel

- Dining out

Tracking every expense helps identify areas where you can save money.

Step 3: Compare Income and Expenses

If expenses exceed income, reduce unnecessary spending.

The goal is simple:

Income > Expenses

The 50/30/20 Budget Rule

One of the easiest budgeting methods is the 50/30/20 Rule.

Allocate your monthly income like this:

- 50% for Needs

- 30% for Wants

- 20% for Savings and Investments

For example:

Monthly Income = $3,000

Needs = $1,500

Wants = $900

Savings = $600

This method keeps your finances balanced without making budgeting overly complicated.

Learn more here:

https://www.consumerfinance.gov/

Building Good Saving Habits

Saving money is one of the most important aspects of personal finance.

The key is consistency.

Even saving a small amount every month creates long-term financial security.

Good saving habits include:

- Pay yourself first

- Automate savings

- Avoid impulse purchases

- Set financial goals

- Save windfalls like bonuses or tax refunds

The Importance of an Emergency Fund

Life is unpredictable.

Unexpected situations happen without warning.

Examples include:

- Medical emergencies

- Job loss

- Home repairs

- Car breakdowns

An emergency fund protects you from relying on debt.

Financial experts recommend saving 3–6 months of living expenses in an easily accessible account.

For example:

Monthly expenses = $2,000

Emergency Fund Goal:

Minimum = $6,000

Ideal = $12,000

Having an emergency fund provides peace of mind and financial stability.

Common Money Mistakes Beginners Should Avoid

Everyone makes financial mistakes, but learning from them early can save thousands of dollars.

1. Living Beyond Your Means

Buying things you can’t afford often leads to debt.

Live below your income whenever possible.

2. Ignoring a Budget

Without a budget, money tends to disappear quickly.

Track every expense.

3. Not Saving Early

The earlier you start saving, the more your money grows over time.

Time is one of the biggest advantages in personal finance.

4. Depending on Credit Cards

Credit cards are useful when used responsibly.

However, carrying high-interest balances can create long-term financial problems.

Always try to pay the full balance every month.

5. Not Setting Financial Goals

Without goals, it’s difficult to stay motivated.

Examples:

- Save $10,000

- Buy a house

- Pay off student loans

- Build an investment portfolio

Clear goals lead to better financial decisions.

Smart Financial Habits to Develop

Successful people often share similar financial habits.

These include:

- Spend less than you earn.

- Save consistently.

- Invest regularly.

- Avoid unnecessary debt.

- Continue learning about money.

- Review your budget every month.

- Increase your income whenever possible.

- Think long-term instead of chasing quick profits.

Small daily habits often create life-changing financial results.

Managing Debt Wisely

Debt is a common part of modern life, but not all debt is bad. The key to good personal finance is understanding how to manage debt responsibly.

There are two main types of debt:

Good Debt

Good debt can help improve your financial future. Examples include:

- Student loans

- Home mortgages

- Business loans

These types of debt may increase your earning potential or build valuable assets over time.

Bad Debt

Bad debt usually comes from buying things that lose value quickly or making unnecessary purchases with borrowed money.

Examples include:

- High-interest credit card debt

- Payday loans

- Unnecessary personal loans

- Buy-now-pay-later purchases you can’t afford

The goal isn’t to avoid debt completely—it’s to borrow responsibly and pay it back on time.

For more information about managing debt, visit:

https://www.consumerfinance.gov/consumer-tools/debt-collection/

Strategies to Pay Off Debt Faster

If you’re dealing with multiple debts, consider one of these proven strategies:

1. The Debt Snowball Method

This strategy focuses on paying off the smallest debt first while making minimum payments on the others.

Once the smallest balance is paid off, move to the next one.

This approach builds momentum and keeps you motivated.

2. The Debt Avalanche Method

This method focuses on paying off the debt with the highest interest rate first.

Although progress may seem slower at first, you’ll usually save more money on interest over time.

Choose the strategy that best matches your personality and financial goals.

Understanding Credit Scores

A credit score is a number that represents how responsibly you manage borrowed money. Lenders use it to determine whether you’re likely to repay a loan.

A good credit score can help you:

- Qualify for loans more easily

- Receive lower interest rates

- Get approved for credit cards

- Rent an apartment

- Secure better insurance rates in some countries

Several factors influence your credit score, including:

- Payment history

- Credit utilization

- Length of credit history

- Types of credit accounts

- New credit applications

The best way to improve your credit score is to pay bills on time and avoid carrying high credit card balances.

To learn more about credit scores, visit:

https://www.experian.com/blogs/ask-experian/

Investing for Beginners

Saving money is important, but investing allows your money to grow over time.

Investing means putting your money into assets that have the potential to increase in value.

While all investments carry some level of risk, long-term investing has historically helped many people build wealth.

Common Investment Options

Stocks

When you buy stocks, you own a small portion of a company.

Stocks can offer high returns over time, but they also come with higher risk.

Bonds

Bonds are loans made to governments or companies.

They generally offer lower returns than stocks but are considered less risky.

Mutual Funds

Mutual funds pool money from many investors and invest in a diversified portfolio.

They’re a good option for beginners who want professional management.

Exchange-Traded Funds (ETFs)

ETFs are similar to mutual funds but trade like stocks on the stock market.

They often have lower fees and provide instant diversification.

Real Estate

Investing in property can generate rental income and long-term appreciation.

However, it usually requires more capital and ongoing maintenance.

To explore investing basics, visit:

https://www.investor.gov/introduction-investing

The Power of Compound Interest

One of the most important concepts in personal finance is compound interest.

Compound interest means you earn interest not only on your original investment but also on the interest you’ve already earned.

For example:

- Invest $200 every month.

- Earn an average annual return of 8%.

- Continue for 30 years.

Over time, your investment can grow significantly because your earnings generate additional earnings.

Starting early gives your money more time to compound.

Planning for Retirement

Retirement may seem far away, but the earlier you start planning, the easier it becomes.

Even small monthly contributions can grow into a substantial retirement fund over several decades.

Some common retirement accounts include:

- 401(k) plans (United States)

- Individual Retirement Accounts (IRAs)

- Employer-sponsored pension plans

- Private retirement savings accounts

If retirement accounts in your country differ, look for tax-advantaged investment options available locally.

A good rule of thumb is to start saving for retirement as soon as you begin earning an income.

Why Insurance Matters

Insurance is often overlooked, but it’s an essential part of personal finance.

It protects you from major financial losses caused by unexpected events.

Common types of insurance include:

Health Insurance

Helps cover medical expenses and hospital bills.

Life Insurance

Provides financial support for your family if something happens to you.

Auto Insurance

Protects against vehicle-related accidents and damages.

Homeowners or Renters Insurance

Covers damage to your home or personal belongings.

Choosing the right insurance depends on your personal circumstances, family responsibilities, and financial goals.

Tax Planning Basics

Taxes affect almost every financial decision you make.

Good tax planning can help you legally reduce your tax burden and maximize your savings.

Some simple tax planning tips include:

- Keep accurate financial records.

- Save receipts for deductible expenses.

- Understand tax deadlines.

- Take advantage of eligible tax deductions and credits.

- Contribute to tax-advantaged retirement accounts where available.

For official tax guidance in the United States, visit:

If you live outside the U.S., consult your country’s tax authority for accurate information.

Setting Financial Goals

Without goals, managing money becomes much harder.

Clear financial goals help you stay motivated and make better spending decisions.

Short-Term Goals

Achievable within one year.

Examples:

- Build a $1,000 emergency fund.

- Pay off a credit card.

- Save for a vacation.

- Buy a new laptop.

Medium-Term Goals

Usually take one to five years.

Examples:

- Purchase a car.

- Start a business.

- Save for a wedding.

- Complete higher education.

Long-Term Goals

Require five years or more.

Examples:

- Buy a house.

- Retire comfortably.

- Become financially independent.

- Build a diversified investment portfolio.

Write down your goals and review them regularly to track your progress.

Best Personal Finance Apps

Technology makes managing money easier than ever.

Here are some popular personal finance apps:

1. Mint

Helps track spending, budgets, and financial goals.

2. YNAB (You Need A Budget)

Excellent for zero-based budgeting and improving spending habits.

3. Empower Personal Dashboard

Allows users to track investments and net worth.

4. PocketGuard

Helps users avoid overspending by showing how much money is available after bills and savings.

Choose the app that best fits your financial habits and goals.

Personal Finance Tips for Beginners

If you’re just starting your financial journey, these simple habits can make a significant difference:

- Create a monthly budget and stick to it.

- Save before spending.

- Avoid lifestyle inflation as your income grows.

- Build an emergency fund.

- Pay credit card balances in full whenever possible.

- Invest consistently for the long term.

- Learn about money every month.

- Review your financial progress regularly.

- Diversify your investments instead of relying on a single asset.

- Stay patient—building wealth takes time.

Remember, successful personal finance is built through consistency, not perfection.

Frequently Asked Questions (FAQs)

What is personal finance?

Personal finance is the process of managing your income, expenses, savings, investments, insurance, taxes, and financial goals to achieve long-term financial stability.

Why is personal finance important?

Personal finance helps you reduce financial stress, avoid unnecessary debt, build wealth, prepare for emergencies, and achieve life goals like buying a home or retiring comfortably.

How much should I save every month?

A common recommendation is to save at least 20% of your monthly income, but any amount saved consistently is a positive step toward financial security.

Should beginners invest?

Yes. Beginners should start investing as early as possible, even with small amounts, while focusing on diversified, long-term investments.

What is the best budgeting method?

The 50/30/20 Rule is one of the simplest and most effective budgeting methods for beginners because it balances needs, wants, and savings.

Conclusion

Mastering personal finance is a lifelong journey, not a one-time task. The sooner you begin learning how to budget, save, invest, and manage debt, the stronger your financial future will become.

Financial success doesn’t depend solely on how much money you earn—it depends on how wisely you manage what you have. By creating a realistic budget, building an emergency fund, investing consistently, protecting yourself with insurance, and setting meaningful financial goals, you can establish a solid foundation for long-term financial well-being.

Remember that every small financial decision matters. Saving a little today, avoiding unnecessary debt, or investing regularly may seem insignificant now, but these habits can lead to remarkable results over time. Stay patient, continue learning, and adjust your financial plan as your life and goals evolve.

Whether your dream is to become debt-free, buy your first home, travel the world, or retire comfortably, the roadmap begins with a single step. Start today, stay consistent, and let smart personal finance habits guide you toward lasting financial freedom.

For more: click here